【半導體系列文】記憶體的價值:解密 Kioxia 奪冠之路,以及日本「市值龍頭」的權力更迭 | Taisa的對策

鎧俠(Kioxia)挑戰 Toyota 日本股王地位的背後,不只是 AI 記憶體熱潮,更反映日本資本市場正從汽車工業轉向 AI 基礎建設。從東芝拆分、NAND 發明者舛岡富士雄,到台日半導體供應鏈的新聯盟,重新理解日本半導體復興的真正意義。

這幾天,日本財經界的氣氛呈現出顯著的結構性轉變。在東京證券交易所的掛牌企業中,市場討論的核心已從長期領先的汽車龍頭豐田(Toyota),轉向 2024 年底才正式上市的半導體巨頭——鎧俠(Kioxia)。

自掛牌以來,鎧俠在不到兩年的時間內股價增長近 8 倍。目前市場最受關注的預測指出,鎧俠的市值極有可能在 2026 財年結束前挑戰豐田,競爭日本市值第一的寶座。對於長期由傳統製造業主導的日本經濟而言,這種從「引擎與鋼鐵」向「數據儲存」的重心移轉,無異於一場產業板塊的深度位移。今天就來跟大家聊聊這間承襲東芝技術血脈、被譽為「日本記憶體最後希望」的企業,究竟如何在 AI 浪潮下翻轉局勢。

■ 日本半導體的版圖重組:鎧俠的生存與再生

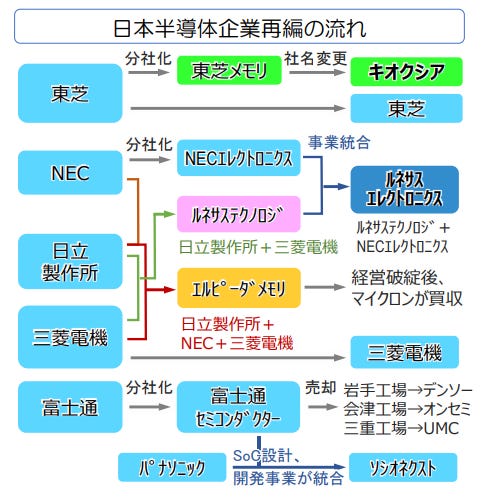

日本半導體產業自 1980 年代的全球巔峰後,經歷了長達數十年的劇烈洗牌。為了應對南韓與美國對手的崛起,日本各大電機巨頭紛紛進行事業再編,將半導體部門分拆、整合或轉手。其中,鎧俠(Kioxia) 的前身正是「東芝記憶體」。2017 年,母公司東芝因受美國核電業務巨額虧損拖累,為了填補財務黑洞,不得不將獲利最豐厚的記憶體事業部獨立分拆。這間隨後在 2019 年更名為鎧俠的公司,不僅繼承了東芝的核心技術能量,更在擺脫傳統官僚體制與財務包袱後,成為現今日本在 NAND 快閃記憶體領域唯一的全球級競爭者。

■ 發明者的詛咒:舛岡富士雄與 NAND 的悲劇宿命

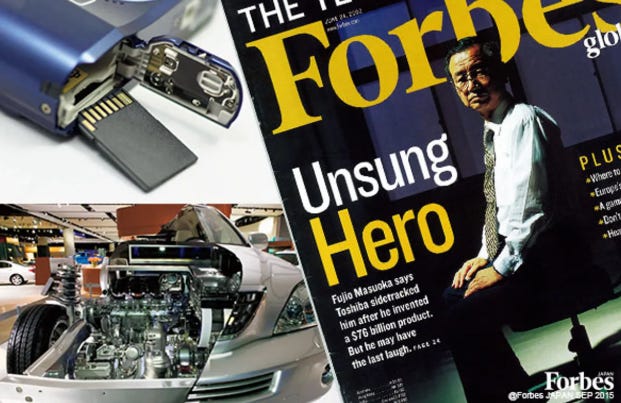

鎧俠的技術血脈,最早可追溯至一位長期被體制忽視的英雄——舛岡富士雄。1980 年代,任職於東芝的舛岡發明了徹底改變資料儲存方式的 NAND 快閃記憶體,這項技術如今是 SSD 與 AI 伺服器的核心。然而在當時,這項突破卻因威脅到獲利極佳的 DRAM 業務,被東芝高層視為「破壞獲利」的異類,舛岡本人也因此遭到冷凍。

儘管 NAND Flash 後來創造了千億美金的產業價值,東芝當年僅發放數百美金的獎金給舛岡,並將其調任至沒有預算與部下的虛職。這段「發明者的詛咒」直到 2017 年東芝因財務危機被迫剝離記憶體部門後才迎來轉機。Forbes曾經特別報導過這位「被忘掉的英雄」,關於他的更多故事歡迎大家可以去看更多,瞭解這位現在仍然再日本學術界活躍的傳奇技術者。

2019 年更名為「鎧俠(Kioxia)」後,公司徹底擺脫了官僚束縛。如今鎧俠衝上 25 兆日圓的市值巔峰,不僅是商業上的成功,更像是一場跨越四十年的歷史復仇,為當年的先知完成了一場遲來的正義。

■ 為什麼是現在?AI 時代開始讓「記憶」比「運算」更重要

很多人以為這波 AI 熱潮最大的贏家只有 GPU。但實際上,AI 資料中心現在真正開始出現瓶頸的,反而是「資料讀寫與儲存速度」。當大型語言模型(LLM)的參數規模持續暴增之後,市場逐漸發現:即使 GPU 再快,如果資料無法高速供應,整體效能依然會被拖垮。這也是近年半導體業界開始高度討論「Memory Wall(記憶體牆)」的原因。

「記憶體牆」(Memory Wall)是指處理器(CPU/GPU)運算速度遠快於記憶體(DRAM)資料存取速度,導致計算單元常需空轉等待數據,形成制約整體效能的瓶頸。在AI時代,因模型規模暴增,此問題日益嚴重,主要因頻寬與容量增長遠落後算力提升。而這正好讓鎧俠(Kioxia)重新回到市場焦點。

過去 NAND Flash 與 SSD 常被視為相對成熟的零組件,但在 AI 時代,高速、大容量、低功耗的企業級 SSD,開始變成 AI 基礎建設不可或缺的一部分。尤其 AI Server 對資料吞吐量的需求遠高於過去傳統雲端架構,讓高階 3D NAND 的重要性快速上升。鎧俠目前主力推進的 218 層 3D NAND 技術,也因此重新被市場評價。另一個容易被忽略的變化,則來自汽車產業。當自動駕駛逐漸進入 Level 4 之後,汽車本身正在快速「伺服器化」。大量感測器、即時影像、AI 判斷與車載系統,都需要更高階的記憶體架構支撐。

■ 日本股市主角交替:從「燃油引擎」到「矽晶圓與金流」的版圖大位移

如果把鎧俠(Kioxia)這波股價上漲放到更大的時間軸來看,其實會發現,這已經不只是單一公司的題材,而是整個日本股市主角正在改變。十年前,日本市值排名前段的企業,核心仍然是汽車、電信與傳統製造業。Toyota、NTT、Honda、Nissan 幾乎代表了當時日本經濟的象徵。但到了 2026 年,日本資本市場開始明顯轉向「AI 與半導體供應鏈」。

最具代表性的,就是東京威力科創(TEL)從 2016 年僅排名 88 名,一路衝進日本前五大企業;而鎧俠(Kioxia)也在 AI 記憶體需求爆發後,快速進入日本核心權值股行列。相反地,過去象徵日本工業時代的 Nissan,市值則大幅滑落,甚至跌出市場主流視野。

這背後反映的,其實是資本市場評價邏輯的改變。過去市場重視的是「能賣多少台車」。但現在市場開始重新定價的,變成「能不能支撐 AI 基礎建設」。而鎧俠剛好就站在這場轉變的中心。因為 AI 時代需要的不只是 GPU,而是大量高速 SSD、NAND Flash 與資料儲存架構。當全球資料中心開始進入 AI 擴建週期之後,記憶體供應鏈的重要性,也開始被重新放大。

某種程度上,日本股市現在其實正在上演一場非常明確的世代交替:從「燃油引擎的時代」,逐漸走向「矽晶圓與 AI 記憶體」的時代。

■ 結語:比起鎧俠能漲多高,更重要的是日本開始重新相信半導體

當然,從我個人的角度來看,鎧俠(Kioxia)這波市值高速成長,未必代表它真的能長期穩坐日本股王的位置。某種程度上,這裡面仍然有很強的 AI 熱潮與記憶體景氣循環因素。畢竟 NAND Flash 本質上仍屬於半導體供應鏈中的一個重要元件,而不是像 GPU、先進製程或核心 AI 平台那樣擁有絕對主導權的存在。記憶體產業本身也一直是典型波動極大的景氣循環產業。

但即便如此,我認為「鎧俠挑戰 Toyota 長年股王地位」這件事情本身,仍然具有非常強烈的象徵意義。因為這代表日本資本市場的關注焦點,正在第一次如此明確地從傳統汽車工業,轉向 AI 與半導體基礎建設。

某種程度上,這或許可以被視為一個時代轉折點。即使未來鎧俠的市值未必能長期維持,但它仍然讓整個日本社會再次意識到:在下一個十年的全球競爭裡,半導體的重要性,可能已經開始超越過去的燃油車產業。

而從台灣的角度來看,這其實也是一個非常值得關注的訊號。因為當日本重新開始把半導體視為「國家級戰略產業」之後,台日之間的合作關係,未來很可能會比過去更加緊密。從台積電熊本、Rapidus,到記憶體、設備與 AI 資料中心供應鏈,台灣與日本其實正在慢慢形成一種新的產業共同體。某種程度上,AI 時代的亞洲科技競爭,可能已經不再只是單一國家的競賽,而是整條供應鏈之間的聯盟戰。

■ 資料參考 :

KIOXIA 公司網站

半導体宮城縣みやぎ半導体産業振興ビジョン ~半導体生産の重要拠点形成を目指して

Forbes日本の「忘れ去られた英雄」 フラッシュメモリを開発した男、舛岡富士雄

PIVOT 【速報・キオクシア急騰のワケ】

日本経済新聞 日本株の主役、車から半導体・銀行へ 時価総額10兆円クラブ30社に成長

■ 工商時間

最近除了很認真在研究日本半導體與 AI 供應鏈之外,也剛好在第一線看到另一個很有趣的變化。現在很多台灣科技業、ODM、OEM 公司,開始面對的競爭,其實已經不只是「成本」或「產能」問題,而是「能不能跟全球客戶即時協作」。

尤其最近跟不少供應鏈主管聊下來,會發現像 AWS、GM 等國際大廠,已經開始把 Slack Connect 視為標準協作方式。很多時候,真正的差距不再只是技術能力,而是資訊同步速度與跨國協作效率。某種程度上,供應鏈的競爭邏輯,正在從過去的「製造能力」,慢慢轉向「數位協作能力」。

最近也因此很積極在準備這場由 Salesforce 與伊原力科技(MAY4S)一起舉辦的線上研討會,會從實際案例聊聊:

・為什麼全球供應鏈開始重新定義「協作」

・台灣製造業怎麼降低跨國溝通成本

・AI Agent 如何開始進入供應鏈協作流程

・以及台廠下一階段的數位競爭力會是什麼

如果是高科技、製造業、供應鏈相關的朋友,我自己其實蠻推薦來聽聽。很多東西,真的已經不是未來,而是現在正在發生。

📍活動時間:2026/06/03(三)14:00 - 15:00

📍活動方式:Zoom Meeting 線上研討會

—

感謝你讀到這裡。

如果你還沒有訂閱我的電子報,誠摯邀請你加入。我是一位在東京工作的台灣女生Taisa Hsu,在IT/軟體相關行業工作。專注於觀察與分享日本企業的商業模式與案例分析。這份電子報既是我持續學習的筆記,也是我希望與你交流的橋樑。期待透過這些文字,讓彼此在商業學習的路上都有新的收穫。

Adjacent angle: Kioxia enters this rally from a more fragile starting point than the stock chart suggests — the company was in active production cuts as recently as 2022–23, during one of the worst NAND oversupply cycles in a decade. What’s structurally different now is that enterprise SSD demand is a higher-floor, less consumer-dependent market. That’s the real break from the historical pattern — and the reason the capital market re-rating may be more durable than past memory rallies.